The Regulator: Financial Services Regulatory Authority of Ontario (FSRAO)

Auto insurance regulation in Ontario was originally done though the Financial Services Commission of Ontario, but was taken over by the FSRAO when it was founded in 2018.

Mandatory Coverage

Ontario requires all private passenger vehicles (PPV) to be insured with $200,000 of Third Party Liability which encapsulates Direct Compensation, Property Damage, and Accident Benefits. Consumers are also required to have Uninsured Automobile coverage and Underinsured Motorist coverage.

The Industry - Private Passenger Vehicles (PPV)

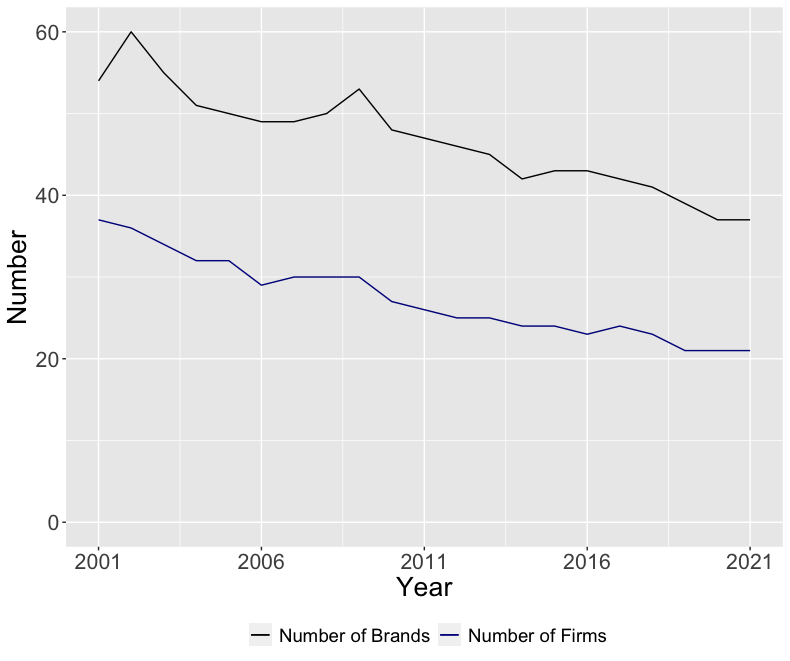

Number of Firms / Brands

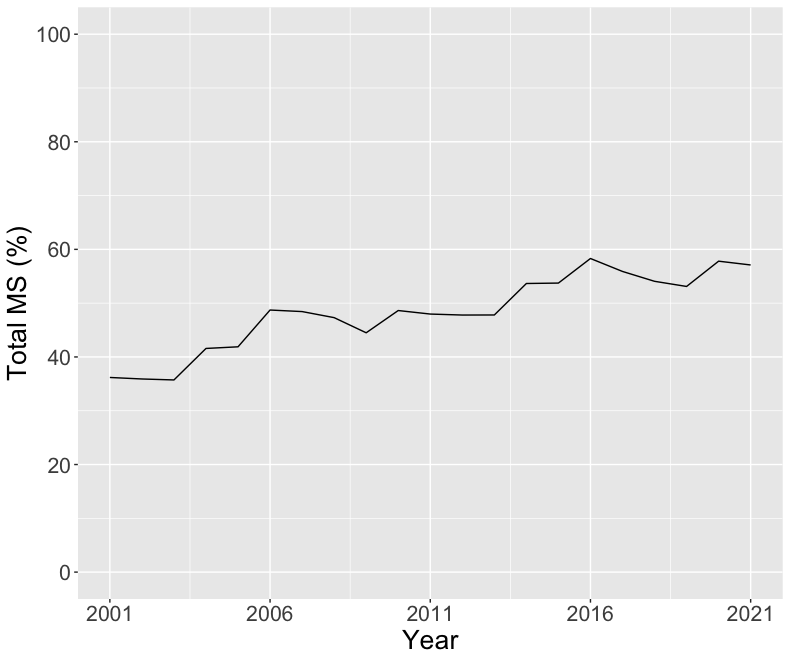

Concentration (C4)

The number of options for Ontarians has declined from 2001 to 2021 has almost half the firms operating in Ontario have been purchased by competitors. Intact insurance alone has purchased five firms during this timeline. The purchasing of firms has also resulted in the brands owned by the firm purchased being integrated into the new owners existing brands.

Given the number of firms declining from 2001 to 2021, the C4 concentration, or the combined market share of the four largest firms has been steadily increasing. The Canadian Competition Bureau begins to consider the activity of an industry once its C4 reaches 65 which given the current trend line I would expect the auto insurance industry in Ontario to do in five years.

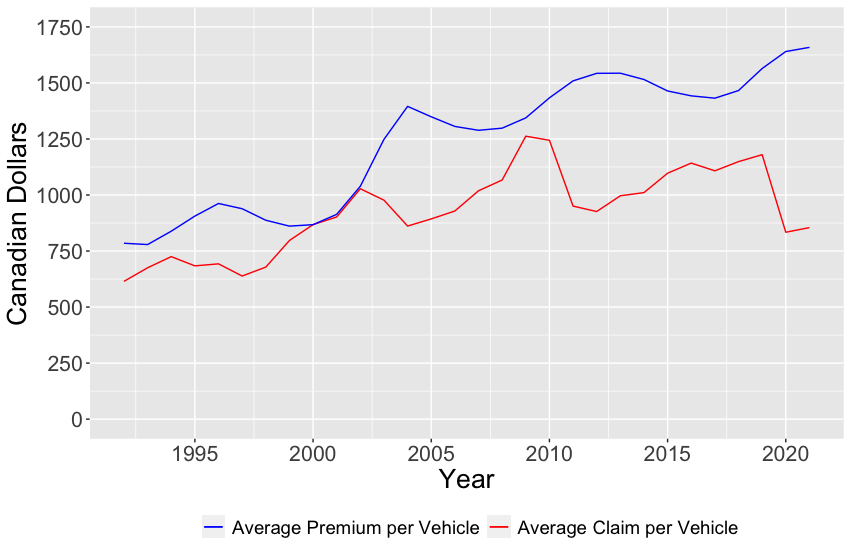

Average Premium and Claims Per Vehicle

Until 2010, average premium per vehicle and average claim per vehicle (all claims paid divided by all vehicles insured) grew together. In 2010, Ontario Regulation 34/10 was introduced capping the payouts for injuries sustained in an accident. The result was a sharp decline in claims paid out in 2011. While premiums have continued to rise in Ontario, the average claim per vehicle has never exceeded its 2010 peak.